You’ve been impacted by the collapse of Shield or First Guardian Master Fund and you want to get your money back – what do you need to do? This page provides information on how to ask for your super back from different financial businesses that were involved in your investment journey.

On this page

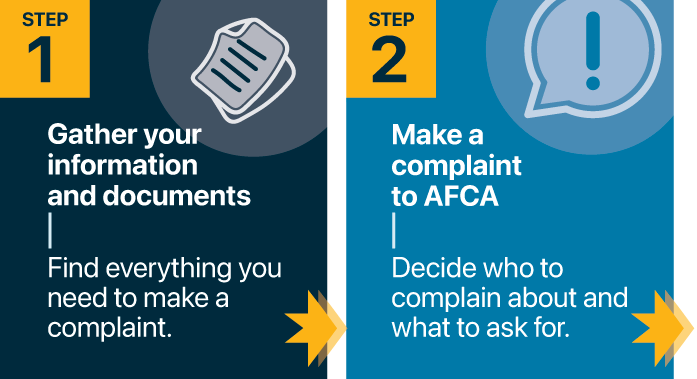

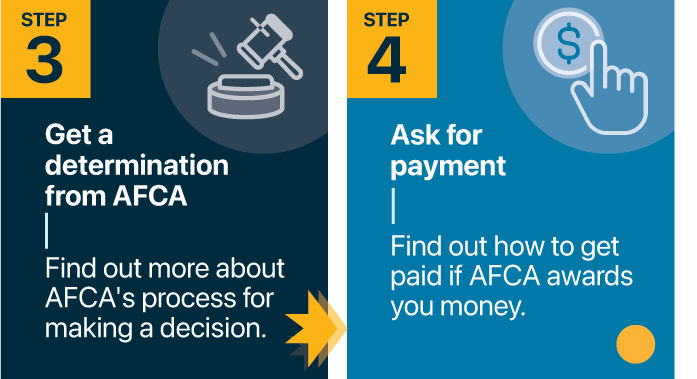

The AFCA complaint process

Most people who have lost money as a result of the collapse of Shield or First Guardian may be able to get some money back. This is because, for most people, it is likely that at least one of the financial businesses they have dealt with has broken the law or failed to do something they should have done causing the investor to lose money.

While there may be other ways to get your super back, making a complaint to the Australian Financial Complaints Authority (AFCA) is free. It is also confidential – AFCA won’t publish your name or tell anyone about your complaint other than the business you complain about.

This page explains the process of making an AFCA complaint as well as important information on who you can complain about, what you can complain about and deadlines for making a complaint. If you have questions after reading the information on this page, read our Frequently Asked Questions.

Not sure where to start? Try our complaint navigator tool to work out who and what you can complain about.

Where can I get more information?

See the links below for more information about each topic.

|

Topic |

Links |

|---|---|

|

Making a complaint to AFCA |

Shield and First Guardian collapse – how AFCA can help Information pack for complainants: examples of documents to provide with your complaint AFCA complaints about First Guardian Master Fund AFCA complaints about Next Generation Advice Pty Ltd |

|

Information about financial advice businesses and advisers |