You might have heard that Shield and First Guardian Master Fund collapsed – but what does that mean? And what actually happened?

On this page

What are Shield and First Guardian?

Shield Master Fund and First Guardian Master Fund are managed investment schemes – a type of fund that holds a range of different investments. People can buy a share of the fund, which is easier and often cheaper than trying to directly buy the individual stock, bonds or other assets the fund is invested in. It’s a lot like buying a sandwich instead of buying a bunch of groceries and making your own.

On the advice of a financial adviser, many people invested their super in these funds through an online investment platform, like a share-trading platform, that lets you or your financial adviser make your own investment mix.

What’s the problem?

Both Shield and First Guardian were closed to new investors and frozen because of concerns about the investments and how the money was being used. Liquidators were appointed to look at the books, find and sell all the assets and pay all the debts.

The liquidators found that neither fund has enough money to pay back investors in full. How much each person will get back depends on a lot of factors, like how much money the liquidators can sell the assets for and the amount of debts that they have to pay. The liquidation process is ongoing and it will take a few years to get it all sorted out.

Based on the information provided by the liquidators, it appears that both funds were not being managed properly and investor money was being misused. The funds were not actually invested the way people were told they were.

Meanwhile, the Australian Securities and Investments Commission (ASIC) is investigating the people responsible for both funds, the marketing lead generators, the financial advice businesses and financial advisers who recommended the funds, the super funds who made Shield and First Guardian available to their members to invest in and other people who were involved.

How did people get into Shield and First Guardian?

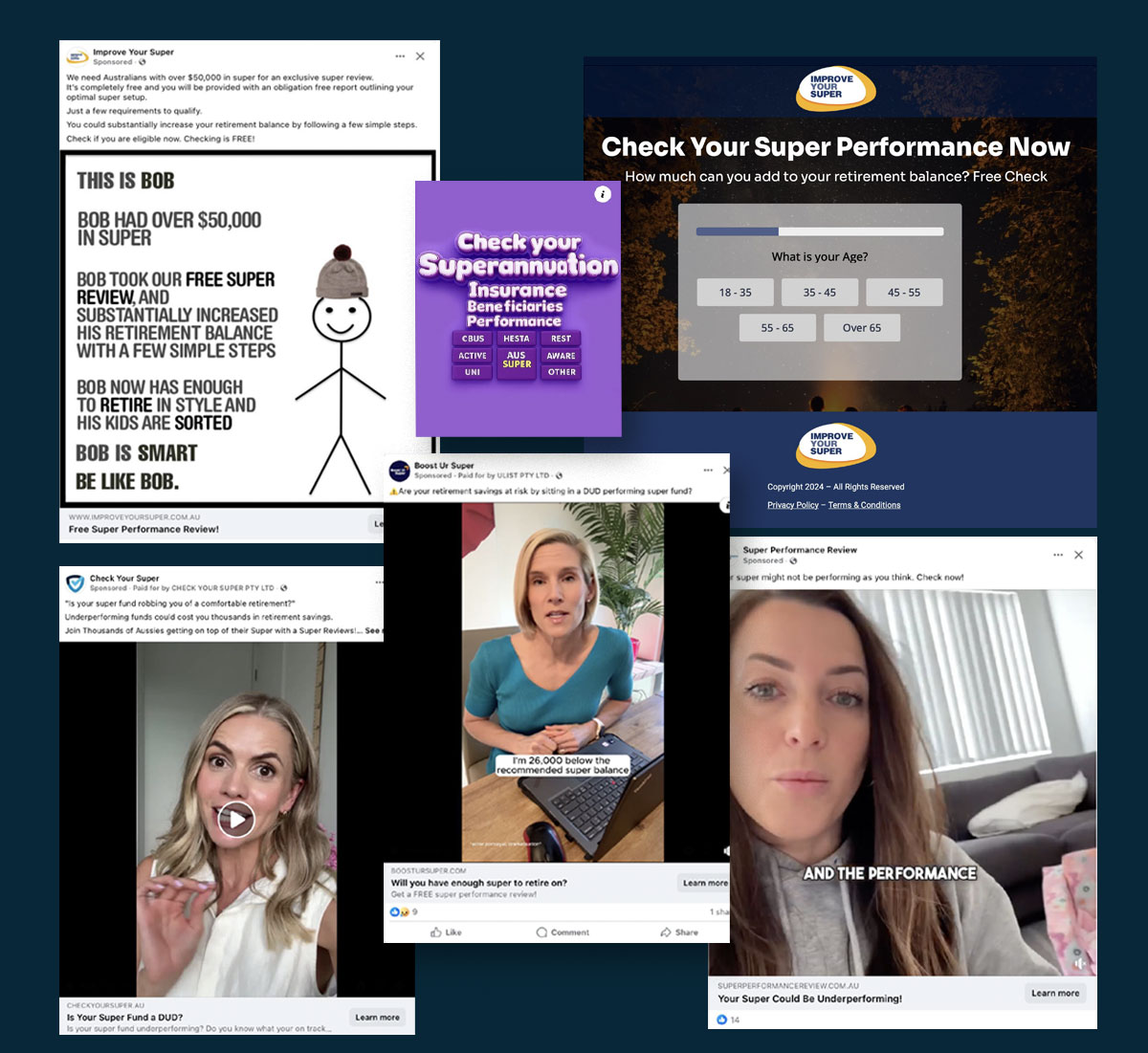

ASIC is still investigating, but so far it looks like many people who invested were contacted by telemarketers known as ‘lead generators.’ While some were cold-called, many clicked on a social media ad offering a free super comparison or review and completed a form with their contact details.

The lead generators referred people to financial advisers who told them they would get better returns if they moved their super to a platform and invested in Shield or First Guardian. People were often told their current funds were not doing well (when they actually were).

Often the adviser would recommend that the person invest all or most of their money in one of these investment schemes, rather than invest in a mix of things. Some people were advised to invest in Shield or First Guardian through a self-managed superannuation fund (SMSF).

Examples of Super Switching Ads

Peter's story

Peter (not his real name) was convinced by a financial adviser to move his super into a platform and invest over $440,000 in First Guardian through a super platform.

“The financial adviser told me that I only have a few years to go until retirement, and it’s better I move into a higher growth account, so I thought ‘he knows what he is talking about, I’ll go with what he says’,” Peter recalls.

Peter, who is 64, has worked in the mining industry for over 20 years. He was looking forward to retirement. “I was hoping that at the end of next year I would be able to retire with a comfortable income,” he says. “But because of the situation I’m in now, I’m scared I might have to work another 20 odd years to get some kind of amount of money to survive on or until I drop.”

He says he is trying to remain patient and let the liquidators’ work and his complaint to the Australian Financial Complaints Authority run its course. “I try not to stress about it, my wife stresses more than me,” he says. “It feels like we are in limbo, I’ve got no idea what the future holds.”

Read more about Peter’s experience.

Shouldn’t people have known Shield and First Guardian were dodgy?

High-risk super switching schemes are very sophisticated. The lead generators and financial advisers involved in selling these schemes sound smart, professional, organised and confident that the new investment will make a lot more money. These lead generators and advisers use a lot of different strategies to convince or pressure people into agreeing to switch their super. For example, they compliment people for taking an active interest in their super and talk about their own and other clients’ gains from investing based on this advice.

Shield and First Guardian were offered on well-known super investment platforms, like the Macquarie Wrap and Netwealth Super platforms. Some people felt reassured that they were investing through a platform with a big name that they trusted.

Most of the time a real financial adviser was involved in providing people with advice to switch into Shield and First Guardian (even if the investor didn’t talk to them directly). Most of those advisers were registered with ASIC to provide personal advice, had completed their education requirements and had no history of being disciplined for giving bad advice.

Many smart, hard-working people were convinced to switch their super through these schemes. They trusted the advice their financial adviser provided and believed that the advice was in their best interests. Because of how professional these schemes are, it would have been very difficult for someone to find out the advice they’d been given wasn’t in their best interests.

Dominik’s story

“I saw an advertisement on Instagram telling me that the government had found some super funds were performing poorly and offered to do a super health check to make sure I wasn’t in one of them,” says Dominik (not his real name). “I signed up and got a call from a superannuation expert with over a decade of experience. I found them on the adviser register, so I knew they were legitimate. They complimented me for taking an active interest in my super at a young age and for the good decisions I’d already made.”

“They took me through all the tips and tricks for making the most of my money. It wasn’t all about how much better off I would be financially if I switched funds, some of it was about how to protect my loved ones if I couldn’t work or passed away.”

“They talked to me about real concerns I had about how well my super fund was doing. They raised the fact that despite managing hundreds of thousands of my savings over many years, I’d never once had a call from my fund, which was a good point. Overall they made me feel like I was doing a really good thing for me and my family by thinking about my super.”

Isn’t super meant to be safe?

Super funds offer different types of products. Most products have a lot of protections, including an annual performance test by a regulator. If a product fails the performance test once, the fund has to let you know. If it fails a second time, the fund isn’t allowed to take on new members until it can solve the problem, usually by merging with a better fund. This is an important consumer protection, which forces super funds to fix poor performance and inform consumers when the fund has failed the test.

Platforms, like the ones with Shield and First Guardian on their menus, are different.

Products that super funds offer through platforms, but don’t design themselves, are not tested. Super trustees still have obligations when choosing which products to make available and to keep an eye on them over time. ASIC has taken two super funds to court, saying they breached their obligations by not protecting people from these products.

Some super funds have relied heavily on financial advisers to decide what investments are right for people to invest in. If your financial adviser is recommending you move into a platform product, it’s really important to ask them questions so you understand all the possible benefits and risks before committing.

Self-managed superannuation funds (SMSFs), funds that you run yourself, are only as safe as the investment decisions you make. SMSFs give you a lot more control over your own money, but they don’t have many of the protections that regular super funds have. It’s up to you and your financial adviser to make the right choices. Again, it’s really important to ask questions of your financial adviser before deciding if an SMSF is right for you.

- Find out more about how to protect yourself from high risk super switching schemes.

- Find out more about how to choose a good financial adviser.

Where can I get more information?

See the links below for more information about each topic.

|

Topic |

Links |

|---|---|

|

ASIC’s investigation into what happened |

ASIC’s investigation into Shield Master Fund |

|

ASIC’s review of high risk switching schemes |